Hire Purchase Services: A Practical Way to Own Business Assets

Running a business is expensive. Whether you’re a startup trying to get your first delivery van on the road or a seasoned manufacturing firm looking to upgrade to a high-tech CNC machine, the “price of admission” can be a total gut punch.

You see the equipment you need, and you see the price tag; suddenly, your bank account looks a little… shy. This is where hire purchase services step into the spotlight.

Think of it as the ultimate “middle ground” between renting something forever and dropping a massive pile of cash all at once. It’s a practical, tried-and-tested way to get the assets you need today while paying for them as they actually generate money for you.

In this guide, we’re going to break down how hire purchase works, why it might be the smartest move for your balance sheet, and how to navigate the process without getting a headache.

What Are Hire Purchase Services?

In the simplest terms, Hire Purchase is a finance solution where you pay for an asset in installments over a set period. Here’s the “kicker” that defines HP: you use the item immediately, but you don’t technically own it until the very last payment is made.

Think of it like a “rent-to-own” agreement for grown-ups and businesses. You put down an initial deposit, followed by regular monthly (or quarterly) payments. Once that final check clears, the title transfers to you, and the asset is 100% yours.

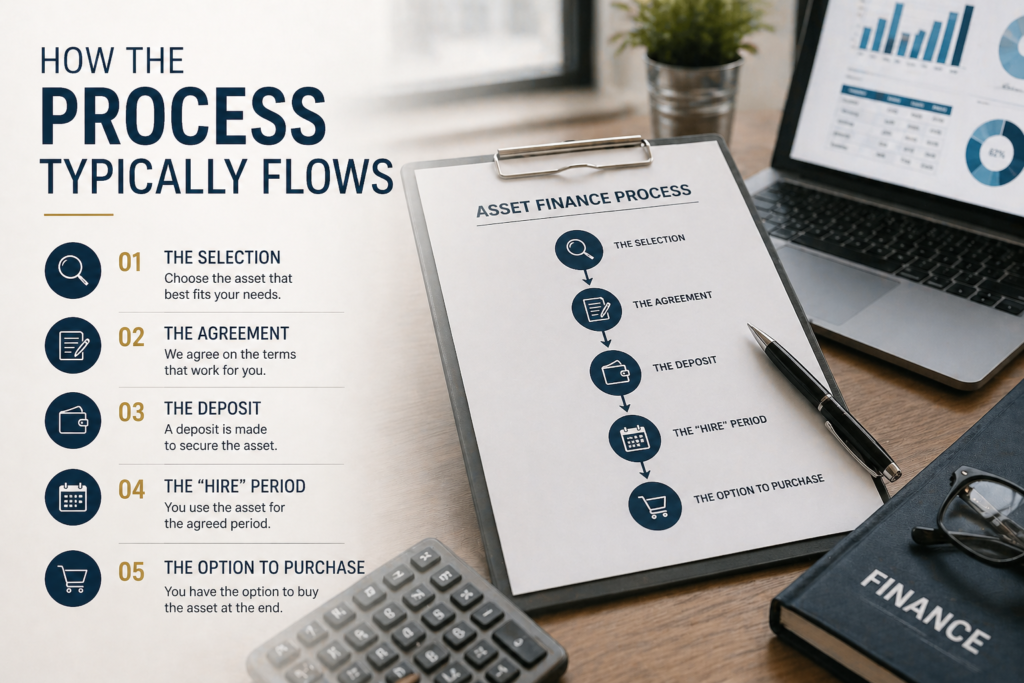

How the Process Typically Flows

- The Selection: You find the asset you need—be it a tractor, a fleet of laptops, or a commercial oven.

- The Agreement: You partner with a provider of Hire Purchase Services. They buy the asset from the vendor on your behalf.

- The Deposit: You usually pay a percentage of the total cost of the machinery or equipment upfront (typically 10% to 20%).

- The “Hire” Period: You pay fixed installments over 1 to 5 years. During this time, you have full use of the equipment, but the finance company is the legal owner.

- The Option to Purchase: At the end of the term, you pay a small, nominal “option to purchase” fee. Congratulations—the asset is now officially on your books!

Why Businesses Prefer Hire Purchase Services

Why bother with hire purchase when you could just get a bank loan or lease? It comes down to certainty and ownership.

1. Conservation of Cash Flow

- Cash is the lifeblood of any business. If you spend $50,000 upfront on a new piece of machinery, that’s $50,000 you can’t use for marketing, hiring, or emergencies.

- With hire purchase services, you spread that cost out. You keep your working capital “liquid” while the machine starts paying for its own installments by increasing your production.

2. Fixed Interest Rates

- Most hire purchase agreements come with fixed interest rates. In an economy where rates can bounce around, having a fixed monthly outgoing is a massive win for budgeting.

- You know exactly what’s leaving your account on the 1st of every month for the next three years. No surprises.

3. Tax Efficiency

- Even though you don’t “legally” own the asset until the end, for tax purposes, you can often claim capital allowances from the start of the agreement. You can also usually deduct the interest element of your monthly payments as a business expense.

4. Total Ownership

- Unlike a standard lease, where you might have to hand the keys back at the end of the term, hire purchase is a path to ownership. For assets that have a long lifespan (like heavy machinery or vehicles), it is often the most cost-effective route in the long run.

Is There a Catch?

It wouldn’t be a fair guide if we didn’t look at the loopholes. Hire Purchase Services aren’t a “magic wand.”

- Total Cost: Because you’re paying interest, you will end up paying more for the asset than if you’d bought it outright with cash.

- Commitment: You are locked into the agreement. If your business direction changes and you no longer need the asset, ending the contract early can sometimes be costly.

- Maintenance is on You: Unlike some operating leases, you are usually responsible for the maintenance and insurance of the asset from day one. If the machine breaks down, you still have to make the payments.

Hire Purchase vs. Leasing: Which is Your Style? in 2026

People often use “leasing” and “hire purchase” interchangeably, but they are different beasts.

| Feature | Hire Purchase | Finance Lease |

| End Goal | Ownership of the asset. | Return or “secondary” rental. |

| Ownership | Transfers to you at the end. | Remains with the lessor. |

| Balance Sheet | Appears as an asset/liability. | Usually appears on the balance sheet. |

| Tax Treatment | Capital allowances available. | Payments are tax-deductible. |

If you want to keep the equipment for 10 years, Hire Purchase Services are usually the way to go. If you want to swap for a new model every 3 years (like with tech), a lease might be better.

Tips for Choosing a Provider

Not all hire purchase services are created equal. When you’re shopping around, keep these tips in mind:

- Check the “Option to Purchase” Fee: Some providers hide a large fee at the end. Make sure it’s a nominal amount.

- Flexibility: Ask if they can tailor payments to your seasonal cash flow. If you’re a farmer, maybe you want lower payments in winter and higher ones during harvest.

- Speed of Approval: In business, timing is everything. Look for providers known for quick turnarounds so you don’t miss out on a deal for the equipment you need.

Also Read:- Operating Lease Service: How It Works and Who Should Use It

Wrapping Up

At last, Hire Purchase Services are about empowerment. They allow you to dream bigger than your current bank balance. They provide a structured, predictable, and tax-efficient path to building a “kit” of assets that will drive your business forward for years to come.

Instead of asking, “Can I afford this today?” Hire purchase lets you ask, “What could my business achieve if I had this equipment tomorrow?”

FAQs

Q. Can I get hire purchase if I have a new business?

Ans:- Yes, though it might be slightly tougher. Providers might ask for a larger deposit or a personal guarantee since you don’t have a long financial history.

Q. Who is responsible for repairs during the contract?

Ans:- Usually, you are. Since you are the intended owner, the responsibility for keeping the asset in good working order, as well as insuring it, falls on your shoulders.

Q. What happens if I miss a payment?

Ans:- Because the finance company still technically owns the asset, they have the right to repossess it if you default on your payments. Always communicate with your provider early if you’re facing a cash flow crunch.

Q. Can I settle a hire purchase agreement early?

Ans:- Absolutely. Most providers allow for early settlement. You might even save on some interest, though you should check your contract for any “early exit” fees.

Q. Is the VAT paid upfront?

Ans:- In most cases, the full VAT amount of the asset is paid upfront at the start of the agreement (along with your deposit). However, if you are VAT-registered, you can usually reclaim this in your next return.

Discover the Latest Trends

Stay informed with our latest articles and resources.